Reporting on how much consumers will save on health insurance under the American Rescue Plan Act (ARPA) has never been easy, but last week, it got more complicated.

Previous studies on how ARPA would affect household spending on health insurance underestimated the effects of the law, according to a report on Oct. 6 from the Commonwealth Fund. That means consumers could spend much less out of pocket for copayments and deductibles if Congress passes the reforms being debated now under budget deliberations. The increased savings come because of a recalculation of the effects of ARPA, the fund reported.

Although the recalculation didn’t get much coverage, this story is important for journalists because the increased savings could be in the billions of dollars. In addition, the reforms proposed in Congress would cut the number of Americans without health insurance by 7 million, the fund reported.

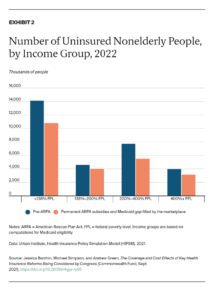

In a report the fund published in September, “The Coverage and Cost Effects of Key Health Insurance Reforms Being Considered by Congress,” researchers from the Urban Institute noted that members of Congress have proposed a budget this year that includes reforming the Affordable Care Act (ACA) in two ways. One reform would make permanent the enhanced premium subsidies in ARPA that otherwise would expire at the end of next year. The other reform would fix what’s called the Medicaid coverage gap by extending eligibility for subsidies on the ACA marketplaces to people earning below 100% of the federal poverty level (FPL) in the 12 states that have not expanded Medicaid.

In those 12 states (Alabama, Florida, Georgia, Kansas, Mississippi, North Carolina, South Carolina, South Dakota, Tennessee, Texas, Wisconsin and Wyoming), Medicaid eligibility for adults is strictly limited. The median annual income limit for a family of three is just 41% of the FPL, or $8,905. Also, childless adults are ineligible.

When Congress passed ARPA last spring, the law temporarily expanded the subsidies consumers get when buying ACA-compliant health insurance on healthcare.gov or their state’s exchange, as we reported in three earlier blog posts: on March 16, April 2, and July 23. Those expanded subsidies improved the ACA’s existing subsidies, limiting what consumers would spend on insurance premiums. That meant that for this year and all of 2022, low-income families got even more financial assistance when buying health insurance and paying their copays and deductibles.

What’s more, ARPA made ACA coverage more affordable for middle income families who previously found ACA coverage too high by limiting what marketplace consumers spend on insurance premiums to 8.5% of income. In other words, both low-income and middle-income families benefited under ARPA.

The problem with ARPA is that some of those reforms are due to expire at yearend 2022. If Congress doesn’t pass the reforms being debated now, costs will rise in 2023, KFF noted in a report last month, “How Marketplace Costs and Premiums will Change if Rescue Plan Subsidies Expire.”

Recognizing that insurance costs will rise, members of Congress have proposed ways to make the insurance savings permanent and included those methods in its current budget negotiations.

In the September report, Urban Institute researchers showed that making the ARPA premium subsidies permanent and eliminating the Medicaid coverage gap would make health insurance more affordable for about 7 million Americans, reducing the proportion of adults without health coverage by about 25% next year. In doing so, the number of adults without health insurance would drop in all states, particularly in the 12 non-expansion states, the researchers noted. At the same time, the premiums consumers pay for ACA-compliant coverage in the marketplaces would drop by 18%, and enrollment in marketplace plans offering subsidies would nearly double, they wrote.

These reforms would increase federal spending by about $442 billion over 10 years and raise the federal deficit by some $333 billion, the researcher added.

While costly for taxpayers, the reforms will also improve household finances for those buying health insurance on the marketplaces. “We estimate that household spending on premiums would fall $8.8 billion in 2022 even as enrollment increases,” the report noted. “Overall, households would save $8.2 billion, according to our estimates.”

The ARPA alone would cut average household spending per enrollee by 23.1%, the report added. Estimating the effect of the proposed changes on the average household, however, would require a separate analysis that has not been done, said researcher Jessica Banthin, a senior fellow in the institute’s health policy center. Such an analysis is challenging because average family spending varies widely depending on health status and how much a family uses the health system, she added.

The savings are nonetheless significant, Sara R. Collins, Commonwealth Fund’s vice president for health care coverage and access told AHCJ.

“This recalculation shows how valuable the cost-sharing reductions are for people who buy health insurance in the marketplaces and are eligible for them, meaning the poorest people in the marketplaces,” she said. “The advantage of having made this error is that you can actually see the large reduction in out-of-pocket spending that people with lower incomes get when buying marketplace plans.”

This blog post touches upon only the highlights of this issue. There is much more detail in these reports:

- “Studies Understated Net Household Savings from Health Coverage Expansions Under Debate in Congress,” email from The Commonwealth Fund, Oct. 6.

- “The Coverage and Cost Effects of Key Health Insurance Reforms Being Considered by Congress,” The Commonwealth Fund (with errata note), Oct. 6.

- “The Coverage and Cost Effects of Key Health Insurance Reforms Being Considered by Congress,” Urban Institute, Sept. 9.

- “Filling the Gap in States That Have Not Expanded Medicaid Eligibility,” The Commonwealth Fund (with errata note), June 30, 2021.