With just over a week to go in June, the Affordable Care Act has already had a very successful month in two important ways.

First, the ACA hit a record for enrollment, topping 31 million Americans since the law went into effect in 2014, according to a report the federal Department of Health and Human Services (HHS) issued earlier this month. And, second, the ACA survived a challenge at the U.S. Supreme Court, as we reported last week.

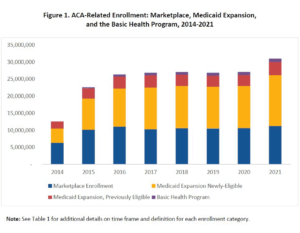

To reach that figure of 31 million, the HHS report included the 20 million who have gained insurance through the marketplaces under the ACA itself and through other ACA insurance programs.

While this news is welcome for more than 31 million Americans and their families, health care journalists still have a lot of explaining to help consumers avoid non-ACA-compliant health insurance plans. Health plans that do not comply with the ACA can leave the unaware with staggering medical bills as a report from 30 patient groups warned in March. (See “Warning from Patient Groups” below.)

“The enactment of the Affordable Care Act in 2010 was the largest expansion of coverage in the U.S. health care system since the passage of Medicare and Medicaid in 1965,” the HHS reported on June 5. Writing for The Washington Post, Amy B. Wang explained that as of February, some 11.3 million Americans were enrolled in ACA plans, and that as of December, about 14.8 million people had enrolled in Medicaid under the law’s rules that allowed 38 participating states and the District of Columbia to expand eligibility for the state-and-federal program.

In addition, 3.9 million Medicaid-enrolled adults benefitted from increased funding, improved outreach and simpler applications under the ACA; and 1 million Americans enrolled in Medicaid under the ACA’s Basic Health Program. This program was for some immigrants and those consumers whose incomes would have made them ineligible otherwise.

Also, some 1.2 million Americans signed up for ACA coverage during the special enrollment period that the Biden administration put in place from Feb. 15 to May 15 (later extended to August 15). We covered that special enrollment period on Feb. 15 when it was announced and then again on March 16.

The eight-page HHS report, “Health Coverage Under the Affordable Care Act: Enrollment Trends and State Estimates,” will be useful for journalists because it explains how the HHS Office of Health Policy reached the 31 million figure and because it includes data on enrollment in each state through the ACA marketplaces (at www.healthcare.gov and in the states) and in Medicaid.

The two main ways the law increased enrollment was by offering tax credits (called Advance Premium Tax Credits) and by providing additional funds so states could expand Medicaid eligibility to adults who have income as high as 138% of the federal poverty level. To date, 12 states have not yet expanded Medicaid eligibility under the ACA, according to this report from KFF. The tax credits helped consumers whose income was between 100% and 400% of the federal poverty level pay for health insurance premiums. In March, the American Rescue Plan expanded eligibility for ACA subsidies for those whose annual income is above 400% of the federal poverty level and raised the ACA subsidies for those with low incomes as we reported at the time.

Warning from Patient Groups

In a recent report, researchers representing 30 patient groups listed eight types of plans that fail to meet the rules of the ACA. As the report showed, non-compliant health plans are sometimes called junk insurance because they can leave unwary consumers with unpaid bills totaling thousands of dollars.

Not only do these plans expose consumers to significant financial risk and surprise medical bills, they also discriminate against consumers who have pre-existing conditions, according to the report, “Under-Covered: How ‘Insurance-Like’ Products Are Leaving Patients Exposed.” Moreover, non-ACA-compliant plans have weakened the ACA by segmenting the risk pool for the individual market and by inflating insurance premiums for those consumers who pay for comprehensive ACA-compliant coverage, the report said.

When seeking to help consumers distinguish between ACA-compliant and non-ACA-compliant plans, journalists have a difficult job because the only way for consumers to get comprehensive coverage that complies with all of the ACA’s rules is to enroll through the ACA marketplaces at www.healthcare.gov, which 36 states use. The 14 other states and the District of Columbia have their own state-operated marketplaces. (See this report from the National Academy of State Health Policy for details on how those 14 states and the District of Columbia have extended ACA enrollment periods.

Consumers shopping online outside the ACA marketplaces will find the nation’s health insurers and health insurance brokers offer ACA-compliant and non-ACA-compliant plans on their websites. While those sites should distinguish between the two types of plans, the distinction may be hard to discern.

When Congress passed the ACA in 2010, it built in consumer protections that required health insurers to cover pre-existing conditions and comply with what the law defined as minimum health insurance benefits. Non-compliant insurance plans do not need to cover pre-existing conditions or include minimum benefits.

For the 26-page “Undercovered” report, the researchers collected data on what is known about the most common kinds of non-compliant plans and makes recommendations for Congress, the administration, and state regulators seeking to add patient protections, particularly for those who have chronic health conditions.

The eight types of non-compliant plans examined in the report are:

- Short-term, limited-duration insurance

- Heath care sharing ministries

- Farm bureau plans

- Grandfathered plans

- Multiple Employer Welfare Arrangements and Association Health Plans

- Spurious single-employer self-insured group health plans

- Minimum essential coverage-only plans

- Excepted benefit plans.

Among the reasons these plans continue to be sold to consumers is a lack of federal and state regulation, the report showed. The researchers called on federal and state officials to revise and strengthen the regulations that govern all of these plans.

The report is available from the Leukemia & Lymphoma Society.