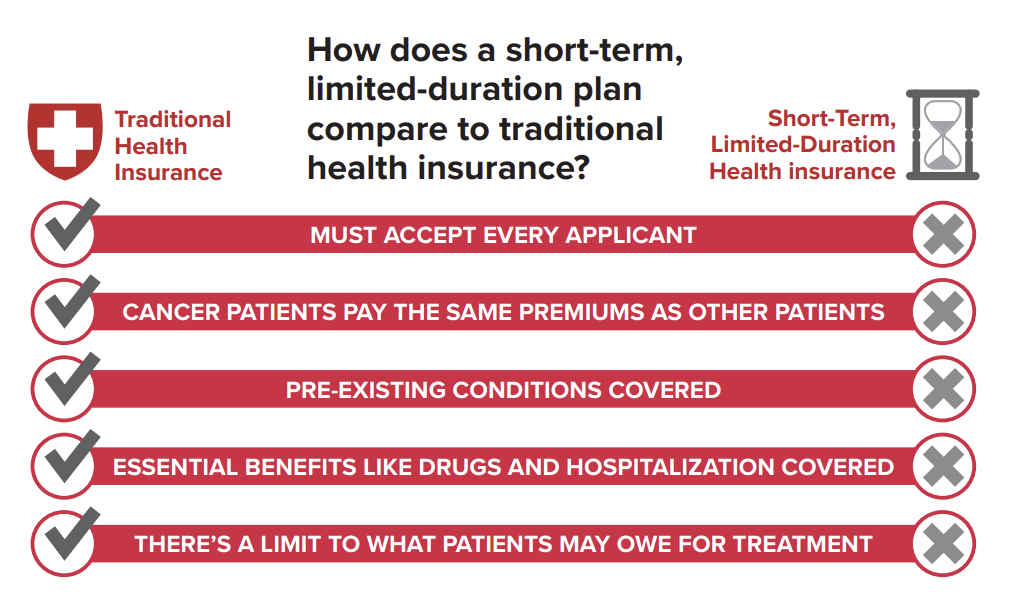

Junk insurance plans that don’t meet the standards of the Affordable Care Act are one of the biggest holes in the patchwork that is the U.S. health insurance system. These plans are typically short-term policies that often discriminate against people with pre-existing conditions and aren’t required to provide coverage for basic services like maternity care, prescription medications and more, according to Aimed Alliance.

To fill this gap and address other weaknesses that harm patients, the federal government proposed new rules in July to protect consumers from junk plans, surprise medical bills and excess costs that lead to medical debt. At the same time, the Biden White House issued a fact sheet detailing these actions.

Why this change is significant

First, junk insurance plans have left consumers with thousands of dollars in unpaid medical bills for years, as many reporters have shown, including Jenny Deam and Maya Miller for ProPublica in 2021 and Sarah Gantz for The Philadelphia Inquirer in 2019. In its fact sheet, the White House linked to Gantz’s harrowing story about a professor who needed an amputation that her junk plan did not cover, burdening her with a $20,000 bill. The Inquirer agreed to make the article available without charge, Gantz wrote in an email.

Second, the proposed rule cuts the maximum term for junk insurance plans from three years to four months. This would reverse a Trump-era regulation passed in 2018, as Robert King reported for Politico in July. The 2018 Trump rule overturned a directive issued under the Obama administration in 2016 that limited short-term plans to three months.

Third, these plans may not offer comprehensive coverage or limit consumers’ costs, and the insurers may not be financially solvent, as Christen Linke Young, J.D., the White House’s deputy director of the Domestic Policy Council for Health and Veterans, wrote in 2020 for the Brookings Institution.

Fourth, junk plans use low premiums to “cherry pick” healthy consumers away from broader and more regulated risk pools, Linke Young explained in the report. “This allows healthy individuals to access lower-cost plans (because they need not pool their risk with sicker people) but drives up costs for everyone that remains in the regulated market,” she added.

Fifth, such plans typically exclude coverage for prescription drugs and mental health, and often are marketed to consumers who do not understand these deficiencies, according to 37 groups representing patients. “This proposed rule would return short-term health plans to their original purpose: a temporary backstop some consumers may purchase while in between health insurers,” reads a July 7 statement from the groups.

Sixth, under the proposed rules, junk plans would need to clearly disclose the limits of their coverage to new and existing policyholders, the White House said.

Improving the No Surprises Act

In addition to proposing new rules governing junk plans, HHS also proposed rules ending what it called abuse of the “in-network” designation under the No Surprises Act. Some health plans contract with hospitals that claim they are not technically part of the insurer’s network, exposing insured patients to higher costs. Under the proposed rule, these providers would be either out-of-network, meaning they must comply with the billing protections of the No Surprises Act, or they are in-network and subject to the ACA’s annual limits on cost-sharing, the White House said.

Also under the proposed rule, hospital facility fees would be treated as if they are normal health care costs. Increasingly, patients are surprised to be charged facility fees when physicians and other providers deliver care outside of hospitals such as in doctors’ offices, the White House said. Health plans and providers would have to disclose information about facility fees under the new rule, the statement added. The White House added that “nonparticipating providers and nonparticipating emergency facilities cannot evade the protections of the No Surprises Act, including the prohibition on balance billing, by renaming charges otherwise prohibited under the No Surprises Act as ‘facility fees.’”

Protections from medical debt

In July, several federal agencies launched an inquiry into costly credit cards and loans pushed onto patients by physicians, hospitals and other providers. Some medical payment companies incentivize providers to enroll as many of their patients as possible by including a share of the revenue or lowering administrative fees. What’s more, providers may be disincentivized to explain legally mandated financial assistance programs or zero-interest repayment options in favor of these high-interest plans.

“Financial firms are partnering with health care players to push products that can drive patients deep into debt,” said Consumer Financial Protection Bureau Director Rohit Chopra in a statement.

A CFPB report in May showed that credit cards and loans for medical care are more expensive for patients than other forms of payment and that they can add to the financial stress of care, decrease access to credit and can lead to collections, litigation and bankruptcy.

Resources

- FACT SHEET: President Biden Announces New Actions to Lower Health Care Costs and Protect Consumers from Scam Insurance Plans and Junk Fees as Part of “Bidenomics” Push. (White House, 2023)

- CFPB, U.S. Department of Health and Human Services, and U.S. Department of Treasury Launch Inquiry into Costly Credit Cards and Loans Pushed on Patients for Health Care Costs (CFPB, 2023)

- Biden reverses Trump-era limits on short-term health plans. (POLITICO, 2023)

- How they did it: Reporting on junk health insurance plans. (AHCJ, 2021)

- Taking a broader view of “junk insurance.” (Brookings Institution, 2020)

- The impact of short-term limited-duration policy expansion on patients and the ACA individual market. (Leukemia & Lymphoma Society, 2020)