Short-term, limited-duration insurance plans threaten the health and financial well-being of American families, according to a recent staff report from Congressional Democrats on the Committee on Energy and Commerce (E&C). The report is a result of an investigation that staff conducted into nine health insurers, including UnitedHealth Group and Anthem, and five insurance company brokers that sell these plans for insurers.

“These plans are simply a bad deal for consumers, and oftentimes leave patients who purchase them saddled with thousands of dollars in medical debt,” according to “Shortchanged: How the Trump Administration’s Expansion of Junk Short-Term Health Insurance Plans is Putting Americans at Risk.” The committee’s investigation into how these plans operate outlines what the report calls “the deeply concerning industry practices” of STLDI plans and the insurance brokers who sell them.

During an AHCJ webinar in May, Sabrina Corlette, a research professor at the Georgetown University ‘s Center for Health Insurance Reform (CHIR), urged health care journalists to ask the departments of insurance in their states about the number of state residents enrolled in these plans. The E&C report provides some information but lacks state-level enrollment data for STLDI plans.

CHIR research fellow Emily Curran earlier this month wrote about the E&C report on the CHIR blog. In “U.S. House Investigation Offers New Evidence on the Dangers of Short-Term Plans,” she outlined some highlights, including how underwriting and rescissions are worse than previously known and how discrimination is rampant, especially against women. A recission is a revocation or cancellation of a health insurance policy that leaves the policyholder uninsured.

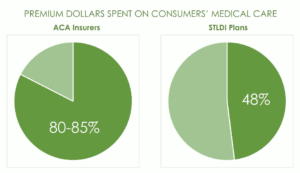

Among many other failings, the E&C report shows how short-term plans can deny coverage for just about any reason, Curran wrote. She added that the report shows that the most frequently cited argument in favor of STLDI plans is that they are affordable, but that argument is false given that enrollees get back only 48 cents for every dollar they spend in premiums.

In a recent interview, Corlette commented on the E&C report, saying that it shows the effects on consumers of deregulating health insurance. Those effects could be disastrous for consumers, especially when the Trump administration and 20 Republican governors are seeking to eliminate the Affordable Care Act in a case before the U.S. Supreme Court.

Late last month, NPR’s Mark Katkov explained that the Trump administration reaffirmed its position in a SCOTUS filing, arguing that the ACA is illegal because Congress eliminated the individual tax penalty for failing to purchase medical insurance. Given that all other provisions of the law are impossible to separate from the individual mandate, it follows then that the rest of the ACA must fall, Katkov added. The court this fall is expected to hear oral arguments in the case, California v. Texas.

In an AHCJ blog post last week, my colleague Joanne Kenen wrote about efforts among Democrats to expand the ACA.

“A big issue in the Supreme Court case is not only the end of the ACA itself but what that would mean for people with pre-existing conditions,” Corlette told me. “That’s why the E&C committee report is timely, because it shows that the Trump administration’s line has been that consumers need not worry.”

The administration says it has an alternative plan if the Supreme Court strikes down the ACA, but neither the administration nor Republicans in Congress have released any details about what’s in that alternative plan, she noted.

“Short-term plans and deregulation are almost certainly part of their plan because short-term plans were one of the top priorities of the Trump administration,” she added. Therefore, the E&C committee’s report explains what the health insurance market might be like in the absence of the ACA, she noted.

The E&C investigation shows that 3 million Americans are enrolled in STLDI plans but that those plans do not provide comprehensive coverage, leaving the insured vulnerable to large bills when they need medical care.

In an article for The Wall Street Journal, Stephanie Armour explained that premiums for these plans are generally lower than premiums for plans that comply with the ACA. STLDI plans can deny coverage based on consumers’ pre-existing conditions and charge women more than they charge men for the same coverage, she wrote, adding that “they also don’t have to cover the same benefits as ACA-compliant plans.”

Many consumers have been forced to pay for their life-saving treatment under shorter-term health plans, Armour added.

Widely available in some states, STLDI plans are banned or their sale restricted in 24 states, the report said. Where they are allowed, they provide coverage for as long as 364 days, and so can be a stop-gap measure for those recently uninsured. So they may be useful to those who lose employer-sponsored insurance during the current coronavirus pandemic. But buyers should be wary because these plans exclude coverage for basic medical services and major medical conditions, the report showed.

One of the strengths of Armour’s reporting is that she explained how enrollment rose sharply in STLDI plans after the Trump administration loosened restrictions on them in August 2018.

More than 600,000 individuals enrolled in the nine health insurers’ plans in 2019, compared with 2018 enrollment, the report said, boosting enrollment from 2.36 million consumers in 2018 to 3 million consumers last year.

Also, brokers increased enrollment of individuals by 60 percent in December 2018 and by more than 120 percent in January 2019, compared with enrollment in previous months. “Enrollment in short-term plans is increasing, at least in part, due to broker incentives to steer consumers away from ACA plans, even if that is what consumer is looking for,” Curran noted.