For an article on short-term health plans, journalist Nancy Metcalf found an ideal source: Stewart Lamotte, a 64-year-old retired restaurateur from Lawrenceville, Ga.

For an article on short-term health plans, journalist Nancy Metcalf found an ideal source: Stewart Lamotte, a 64-year-old retired restaurateur from Lawrenceville, Ga.

In a story that Consumer Reports published in December 2017, “Is Short-Term Health Insurance a Good Deal?”, Metcalf explained that when LaMotte shopped for health insurance, he didn’t qualify for a tax credit under the Affordable Care Act. Also, he balked at the $1,000 monthly premium and a deductible of $6,500 that was required for an ACA-compliant health insurance policy.

“I was looking for major medical catastrophic,” LaMotte told Metcalf. “I wasn’t looking for them to pay for every Band-Aid.”

Instead, he found a short-term plan that cost $261 a month.

You can probably guess what happened next: During a routine dental visit, LaMotte learned he had oral cancer and needed surgery, chemotherapy and radiation, none of which was covered under his short-term policy.

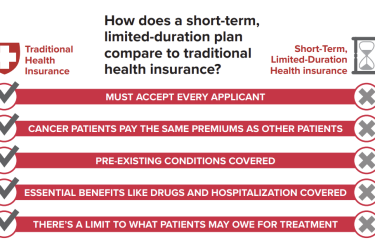

It’s likely there will be many more such stories about consumers like LaMotte, as Laura Newman explains in a new tip sheet about short-term health plans. Newman advises journalists to explain both the benefits (the low monthly premiums) and the risks (these plans do not provide comprehensive coverage).

In a recent article about these plans, Jesse Mignault, a reporter for Foster’s Daily Democrat in Dover, N.H., explained these plans well. He quoted a health insurance broker who said such plans are not for everyone, in part because they do not need to cover the 10 essential health benefits that ACA-compliant plans must cover.

They may not pay for pre-existing conditions, for instance, or prescription drugs, pregnancy or mental health care. And, Mignault added, short-term plans can set limits on lifetime payments. The Daily Democrat published his article, “The risks and rewards of short-term health insurance,” on Jan. 10.

Given that these plans have such limits, consumers should read the fine print carefully, Julie Appleby advised in an article last month for Kaiser Health News, “Short-Term Health Plans Boost Profits For Brokers And Insurers.” That’s where they’ll find the limits of coverage. Even students’ school sports injuries might be excluded, she explained.

While short-term plans are not for all consumers, Appleby added that such plans are good for brokers and for health insurers. Last year the online insurance broker, Ehealth, had an 18 percent increase in enrollment in short-term plans, she reported.

Not only are brokers and insurers enrolling more consumers in these plans, they’re getting a healthy profit from them as well, Appleby added. One broker reported earning 20 percent on the premiums on these plans.

Health insurers will profit too because they will not have to pay as many claims from consumers, she explained. One insurer estimated that 40 percent of its premium income would go to profit, a sizable increase from the limits set under the ACA. The law says health insurers’ profits can be no more than 20 percent of premium income, she added.