When we think of states doing well under the Affordable Care Act, we tend to think of the usual suspects, Democratic leaning states like California, Massachusetts and New York. And it’s true that the states using their own online exchanges for ACA enrollment tend to be the high performers.

What about the states that use the federal platform, Healthcare.gov?

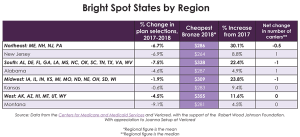

It turns out some are faring a lot better than others, according to a new report from the Robert Wood Johnson’s Kathy Hempstead (who did a webcast with AHCJ a while back) She concludes that the “ bright spots” that stand out in their respective parts of the country are New Jersey, Kansas, Alabama and Montana. That’s based on enrollment, affordability and the degree of insurer participation.

In the Northeast, New Jersey is “relatively well-priced” with bronze plans available for $264 per month for an individual. Competition increased when Oscar Health re-entered the market. For the near future, New Jersey – which now has a Democratic governor – has moved to create a state individual mandate and reinsurance program.

In the Midwest, which includes some “notoriously unsuccessful ACA marketplaces” Kansas did the best (and that despite a very conservative state government) “Premiums increased by 9 percent, and the cheapest bronze plan was below the regional average ($283 versus $309). There were no counties with only one carrier in Kansas, either in 2017 or 2018, and no net change in carrier participation,” Hempstead writes.

In the South, where insurer participation is “sparse,” Alabama was the bright spot, with below average enrollment decline and a more affordable bronze plan option. Most counties in the South have only one insurer, and that’s true in much of Alabama, but not in every county, Along with New Jersey, Alabama did see a bit of net growth in carrier participation.

In the West, Montana is the most affordable, with the best insurer participation, including a rare surviving co-op.

What’s the secret to (relative) success? Each of these states had relatively few people in grandfathered or transition plans – plans that were on the individual market before the ACA and are still permitted. All used “silver loading” to keep prices down after the cost-sharing subsidies were nixed by President Trump. And all have Blue Cross Blue Shield plans with a dominant role and a “historical commitment to serve the individual market.”

Hempstead concludes that the markets are stabilizing – but there are still a lot of questions about insurer participation and premium levels for 2019.